Rental income and any related expenses thereof must always be declared to the Finnish Tax Administration. Relevant information has to be declared even if there is no tax liability after deduction of expenses. If you have several investment properties, you have to provide each apartment’s information separately.

The easiest way to file a tax return is the electronic MyTax service. Pre-completed tax returns are issued at MyTax in March–April each year, after which the tax return should be reviewed and corrected where necessary if the information differs from previously submitted or pre-completed data. The corrections must be completed by the due date specified in the pre-completed tax return.

In addition to assisting you in reviewing the pre-completed tax return, this guide also helps you in completing your tax card or tax prepayment application if you are a first time recipient of rental income. In MyTax, first select ‘Tax cards and prepayment’ and then either ‘Request a new tax card’ or ‘Request tax prepayment’. If you selected the tax card option, choose its complete version next. If you cannot access the electronic services, you can also declare your rental income using a printed form. More information on using a printed form is available on the Finnish Tax Administration’s website here.

1. Log in to MyTax with your banking credentials.

2. In the ‘Individual income tax’ section, go to ‘Tax year 2024’ and select ‘Check pre-completed return’.

3. Next, select ‘Make corrections to details.’

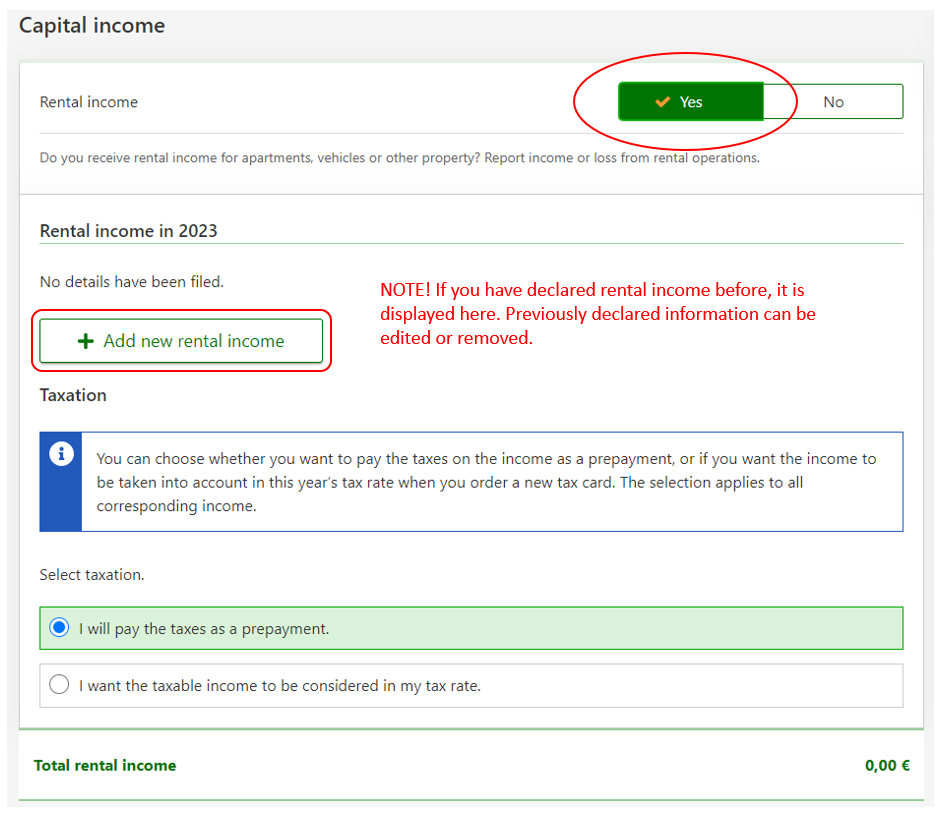

4. Check the background information and the earned income information that are automatically populated on the application. Then, go to the ‘Capital income’ section in the application and under Rental income, first select ‘Yes’ and then click the ‘Add new rental income’ button. If you have declared rental income in previous years, the information is pre-completed in the application.

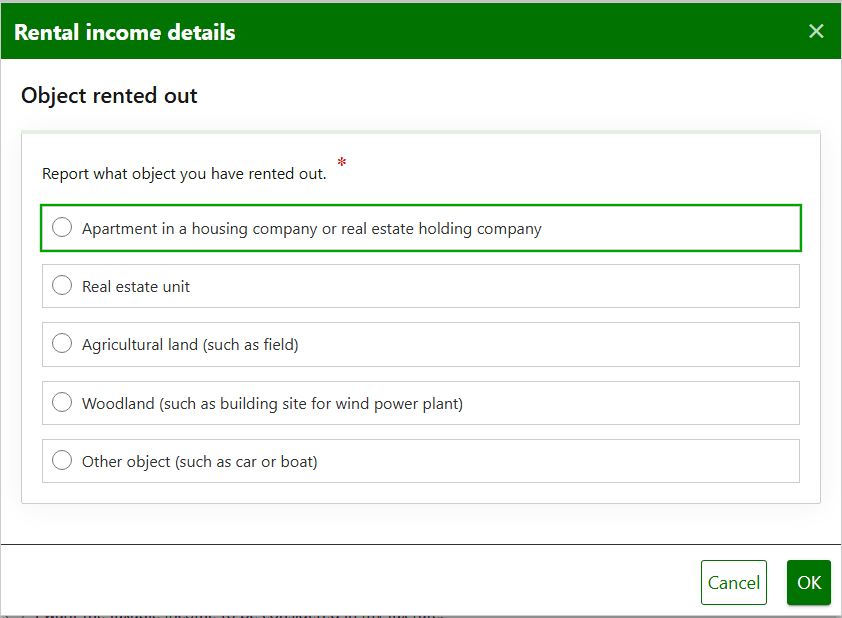

5. Next, choose the type of rented property. Press ‘OK.’

6. If you have leased an apartment in a housing company, enter the relevant information next. If you have declared the same apartment in previous years, its information is pre-completed in the application.

7. Next, enter the information of all tenants that are renting / have rented the property. Also, enter information on the rental income you have received and the expenses related to your rental operation for the particular apartment. Finally, press ‘OK.’

NOTE! Rental income and expenses related to rental activities are divided in taxation according to ownership shares. If you own the apartment jointly with someone else, only report the portion of income and expenses that corresponds to your ownership share. For example, if you own the apartment 50/50 with your spouse, report 50% of the rental income you received together and likewise 50% of all combined expenses for the apartment—regardless of how you actually paid them.

Include in rental income all payments made by the tenant to you, including water charges, even if you pass them on to the housing company. Report the maintenance charges and water fees you paid to the housing company in their own section.

Regarding capital charges, loan repayments, and project contributions, note that they can only be deducted from rental income if they have been recognized as income in the housing company’s accounting. If they have been recorded as reserves in the housing company’s accounting, they are added to the acquisition cost of the apartment and can therefore be utilized in capital gains taxation. You can get information about the accounting treatment of capital charges from the property manager. More information about income recognition and reserving is available here.

For repair expenses, remember that renovations are classified for tax purposes as either annual repairs or improvements. Expenses from annual repairs can be fully deducted in the year they are paid and should be reported in their own section. Expenses from improvements, however, are generally added to the acquisition cost of the apartment. For share-based apartments, improvement expenses can also be deducted as straight-line depreciation over 10 tax years. The annual depreciation portion should be reported under “Other expenses.” Note, however, that expenses for renovations carried out at the time of purchase are always added to the acquisition cost regardless of their nature. More information about deducting renovation expenses in taxation is available here.

Keep a detailed breakdown and receipts for the total amount reported under “Other expenses.” Receipts do not need to be submitted to the Tax Administration, but they may be requested separately, for example, during an inquiry. Receipts and other documentation must be kept for six years from the beginning of the year following the end of the tax year.

Interest on loans taken to generate income can be deducted from capital income in taxation, but for example, interest on investment property loans is not deducted directly from rental income. Instead, they are deducted separately from all capital income. Do not therefore report interest expenses under “Other expenses” when declaring rental income. The Tax Administration receives information about loans and interest expenses directly from your bank. See section 8 of the instructions below.

More information about deductible rental activity expenses is available on our member pages here. It’s also worth reviewing the Tax Administration’s detailed tax guide (available in Finnish and Swedish) on rental income, which answers most questions about deductions.

If needed, the legal advisory service of the Finnish Landlord Association is also available to assist with questions about rental income taxation.

8. Your debt and any interest thereof is displayed in the tax return under ‘Interest on loan’ in the section where income and deductions are pre-completed. Check that your loan has the correct purpose of use and sum. If the information is incorrect, you can change it by clicking on the creditor’s name.

Note! To be entitled to deduct interest requires that your operation is categorized as production of income. If you have leased your apartment to a close relative under current market prices, for instance, the Tax Administration does not categorize the lease as production of income. Therefore, the interest is not tax-deductible.

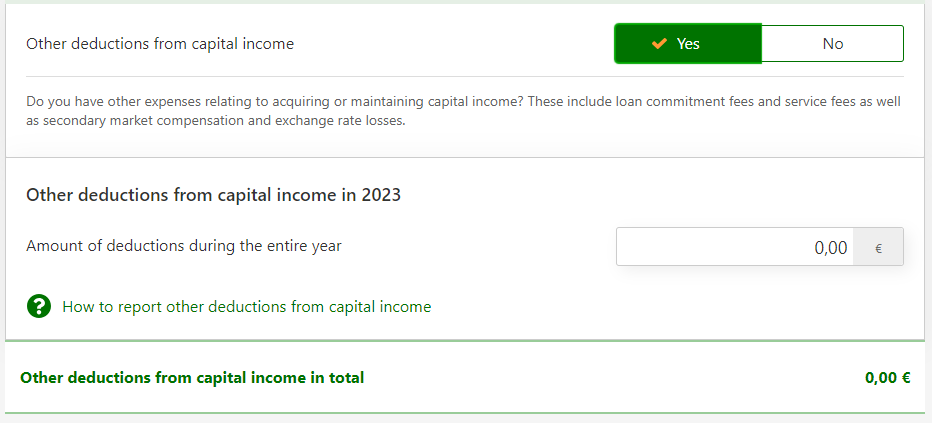

9. Go to ‘Deductions.’ If the pre-completed information includes no other deductions from capital income, go to ‘Other deductions.’ Select ‘Yes’ in ‘Other deductions from capital income.’

Here, you can declare the total sum of other costs related to the production of income that have been incurred not by a specific apartment but by all capital income you have gained. These may include e.g. the membership fee of the Finnish Landlord Association, event related costs and professional literature costs.

10. Review the other sections of your declaration. After you have checked everything, submit the tax return. You may also save an unfinished form and submit it later. However, remember to submit your tax return no later than its due date so that the Tax Administration safely receives your information!